Phone: (407) 476-

Orlando Foreclosure Attorney

Orlando, Florida 32801

Foreclosure Attorney Michael Stites

-

Speak to an Attorney:

Relax. Phone consultations are always free.

Tell Our Attorneys What Happened

Open M -

Orlando FL, 32801

All initial consultations are completely free and we can contact the same or following business day.

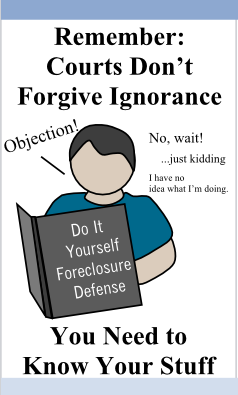

Can I Defend Against a Foreclosure Without a Lawyer?

Find out why the average homeowner generally does not have the resources available to defend against foreclosure without an attorney. The foreclosure defense learning curve is very steep and simple mistakes can have grave consequences.

Most foreclosure defenses surround whether or not the lender followed the correct state foreclosure procedure. You must know what those exact procedures are and how to raise a defense if they were violated. You must also know how to reply to the lender’s foreclosure summons in the correct format, reply to any paperwork the lender’s attorney sends you, file motions in the correct format, and potentially defend your case at trial. If you accidentally do any of it wrong, even if you have a legit reason to fight the foreclosure, the court will not give you any leniency for botching your own case.

Most foreclosure defenses surround whether or not the lender followed the correct state foreclosure procedure. You must know what those exact procedures are and how to raise a defense if they were violated. You must also know how to reply to the lender’s foreclosure summons in the correct format, reply to any paperwork the lender’s attorney sends you, file motions in the correct format, and potentially defend your case at trial. If you accidentally do any of it wrong, even if you have a legit reason to fight the foreclosure, the court will not give you any leniency for botching your own case.

In just about every situation involving a home foreclosure, you will lose your home and probably have a enormous amount of debt if you tackle it by yourself. Some situations are grim even if you hire the best foreclosure defense attorney possible. If the only reason you don’t hire a lawyer is money, remember you will not be paying a mortgage while your home is in foreclosure. You should be able to use some of the money saved to pay for an attorney. Some even offer monthly payment plans to retain their services. If you still can’t afford an attorney, Florida has some free legal services that help you obtain attorneys that work for pro bono (free if your qualify).

Yes but the learning curve is incredibly steep.

Representing yourself in court without an attorney is called Pro Se.

I am a firm believer in the do it yourself method. Most anything can be researched on the Internet and there usually a how-

A Judicial Foreclosure is when a lender sues the borrower to get permission from the court to sell the property to pay for the delinquent loan. In other words, if you get too far behind on your mortgage payments, the lender will sell your home to try to cover the debt you owe them.

Ideally your best defense is to take preventative action before the lender even considers foreclosing on your home. If your monthly payments have started to balloon beyond what you can afford, you will want to contact the lenders loan mitigation department to discuss a loan modification. Negotiations should start as soon as possible. If you lost your job but expect to have another one soon you may want to push for a loan forbearance (delay payment for a few months). There are already a few reasons why the original lender will not usually want to foreclose on you.

You legally have the right to defending against your foreclosure on your own aka “pro se” (representing yourself without an attorney). The real question is should you? Defending a foreclosure is vastly more complicated than fighting a traffic ticket.

Attorneys who specialize in foreclosure defense spend years researching case law, local statues, and previous court rulings. They know how to correctly apply this information when defending a home foreclosure in and out of court.

Let’s say you take the time coming up a reasonable defense strategy. You buy a thick book that tells you all about defending property foreclosures. Maybe you even got a free consultation with a prospective attorney who gave you a helpful brochure. Every year the laws changes. Lawyers must keep up with the changes. The DIY foreclosure books you bought may be outdated. A defense you might have been planning to use may no longer effective depending on what new laws have come out.

To get an idea what you will be dealing with you can start with looking over our article on how to respond to a foreclosure summons. This is usually how a homeowner first finds out that their lender has filed a lawsuit against them and is trying to get court permission to sell their home. In Florida, the homeowner will only have 20 days to respond to the summons. From there you can look into adding affirmative defenses to your response and then learn how and when to file the appropriate motions.

Note: If the borrower was improperly served/was not served you may be able to file a motion to quash instead of responding to the foreclosure summons. Each situation is different.

Quick Foreclosure Overview

")

Created by Attorney Michael Stites & contributing editor Jared Speck

We break down foreclosure procedures into simple to understand terms. Begin here to learn basic steps in foreclosure and what you might be able to do to stop it.

How to Respond to a Foreclosure Summons

Here is how to respond if you get served a foreclosure summons. (What happens when a foreclosure lawsuit is filed against you)

Basic Foreclosure Terminology You must Know

When you have been served a foreclosure summons you may want to understand how to read the legal terms.

Determine If Your Home Foreclosure is Eligible to be Defended

Answer 3 quick questions to see if you have a foreclosure defense case.

Related Topics:

Related Posts:

Consults are free, even if you are asking general foreclosure questions.

Relax. Phone consultations are always free. It can’t hurt to talk.

Speak to an Attorney: